[mEDITate-OR:

not see that what CR is saying to U.S

is almost more important than what CR is showing to U.S.

As you know we, and you should also, follow CR's charts regularly

in part bcuz they are as good as or better than the others.

However, Jim @CR also provides U.S. with explanations that are extremely valuable to our understanding of what the charts are based upon and what they show U.S.

What is too often lost in the "foreclosure" numbers is the effects that that is having on "home ownership".

The following charts show U.S. both of these.

For a total of 7.02 million loans delinquent or in foreclosure.

This suggests there are still about 1.55 million excess housing units.

Not only is there a huge supply of vacant homes...

but there are "incoming" about three times that many.

Ugly.

---------

-------------

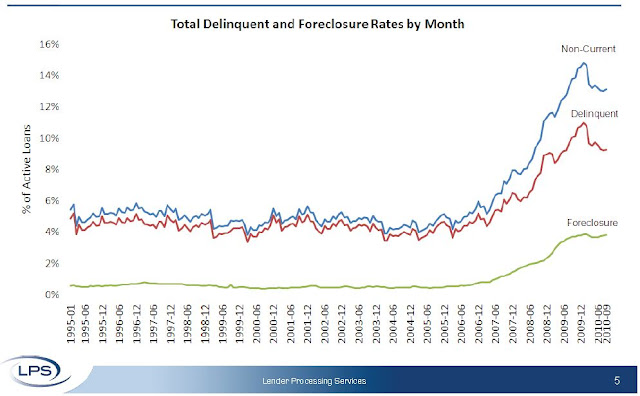

The average number of days delinquent for loans in foreclosure is now 484 days

• In five judicial states (NY, FL, NJ, HI and ME), the average exceeds 500 days

• Over 4.3 million loans are 90 days or more delinquent or in foreclosure

• New problem loans (60+ days delinquent) are back on the rise

---------------

According to LPS, 9.27 percent of mortgages are delinquent, and another 3.84 are in the foreclosure process for a total of 13.11 percent.

It breaks down as:

• 2.64 million loans less than 90 days delinquent.

• 2.32 million loans 90+ days delinquent.

• 2.05 million loans in foreclosure process.

For a total of 7.02 million loans delinquent or in foreclosure.

===============

homeownership:

The homeownership rate was at 66.9%, the same level as in Q2. This is at about the level of early 1999.

The homeownership rate increased in the '90s and early '00s because of changes in demographics and "innovations" in mortgage lending. The increase due to demographics (older population) will probably stick, so I've been expecting the rate to decline to around 66%, and probably not all the way back to 64% to 65%.

------------

The homeowner vacancy rate was at 2.5% in Q3 2010. This is the same level as in Q2, and below the of 2.9% in 2008.

The homeownership rate increased in the '90s and early '00s because of changes in demographics and "innovations" in mortgage lending. The increase due to demographics (older population) will probably stick, so I've been expecting the rate to decline to around 66%, and probably not all the way back to 64% to 65%.

------------

The homeowner vacancy rate was at 2.5% in Q3 2010. This is the same level as in Q2, and below the of 2.9% in 2008.

A normal rate for recent years appears to be about 1.7%.

This leaves the homeowner vacancy rate about 0.8% above normal. This data is not perfect, but based on the approximately 75 million homeowner occupied homes, we can estimate that there are close to 600 thousand excess vacant homes.

--------------

The rental vacancy rate declined to 10.3% in Q3 2010 from 10.6% in Q2.

A normal rate for recent years appears to be about 1.7%.

This leaves the homeowner vacancy rate about 0.8% above normal. This data is not perfect, but based on the approximately 75 million homeowner occupied homes, we can estimate that there are close to 600 thousand excess vacant homes.

--------------

The rental vacancy rate declined to 10.3% in Q3 2010 from 10.6% in Q2.

This decline fits with the Reis apartment vacancy data and the NMHC apartment survey.

This report is nationwide and includes homes for rent.

It's hard to define a "normal" rental vacancy rate based on the historical series, but we can probably expect the rate to trend back towards 8%. According to the Census Bureau there are close to 41 million rental units in the U.S. If the rental vacancy rate declined from 10.3% to 8%, then 2.3% X 41 million units or about 950 thousand excess units would have to be absorbed.

This suggests there are still about 1.55 million excess housing units. These excess units will keep pressure on housing starts, rents and house prices for some time.

This decline fits with the Reis apartment vacancy data and the NMHC apartment survey.

This report is nationwide and includes homes for rent.

It's hard to define a "normal" rental vacancy rate based on the historical series, but we can probably expect the rate to trend back towards 8%. According to the Census Bureau there are close to 41 million rental units in the U.S. If the rental vacancy rate declined from 10.3% to 8%, then 2.3% X 41 million units or about 950 thousand excess units would have to be absorbed.

This suggests there are still about 1.55 million excess housing units. These excess units will keep pressure on housing starts, rents and house prices for some time.

=========

LPS: Over 4.3 million loans 90+ days or in foreclosure

http://www.calculatedriskblog.com/2010/11/lps-over-43-million-loans-90-days-or-in.html

------------

Q3 2010: Homeownership Rate at 1999 Levels

http://www.calculatedriskblog.com/2010/11/q3-2010-homeownership-rate-at-1999.html

==========